|

| Add caption |

Singapore Airlines Ltd (SIA: C6L) is Singapore's national carrier. A large portion of us know about it.

As of late, it was accounted for that Berkshire Hathaway has put resources into American Airlines, Delta Airlines and United Continental.

All things considered, financial specialists might need to know whether we ought to likewise consider putting resources into our banner bearer as well.

Lamentably, there is no simple response to this since financial specialists ought to 1) judge the future business prospects of Singapore Airlines and 2) purchase just if the valuation is correct.

Both undertakings are neither simple nor straight forward.

Here, nonetheless, we will attempt to get a thought by contrasting Singapore Airlines' present cost with book, cost to-income and profit yields in the course of the most recent five years.

As of late, it was accounted for that Berkshire Hathaway has put resources into American Airlines, Delta Airlines and United Continental.

All things considered, financial specialists might need to know whether we ought to likewise consider putting resources into our banner bearer as well.

Lamentably, there is no simple response to this since financial specialists ought to 1) judge the future business prospects of Singapore Airlines and 2) purchase just if the valuation is correct.

Both undertakings are neither simple nor straight forward.

Here, nonetheless, we will attempt to get a thought by contrasting Singapore Airlines' present cost with book, cost to-income and profit yields in the course of the most recent five years.

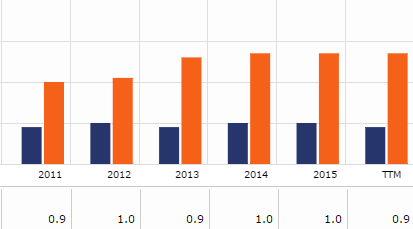

As should be obvious from the outline, the cost to-book proportion for SIA has reliably been somewhere around 0.9 and 1.0 in the most recent five years.

At today's cost of $9.64, the cost to-book proportion is at the lower end of that range.

Put basically, SIA is as of now exchanging at the lower end of its valuation in connection to its five years recorded measurements.

From the outline above, we can see that SIA's P/E proportions have been very unstable, fluctuating between a low of 17.5 times to a high of 66.7 times profit in the most recent five years.

This shows the carrier has a moderately unpredictable acquiring profile, particularly given that it's cost to book proportion has reliably run between 0.9 to 1.0 times.

The TTM P/E proportion of 14.2 shows that SIA is exchanging at its "least" valuation in the previous five years, if the P/E proportion is utilized as a metric.

Profit yield :

Finally, we will look the profit yield. Here, we can see that present profit yield of 4.57% is twice as high as the five-year normal yield.

As we as a whole realize that profit yield is an opposite of valuation. Along these lines, the higher the yield, the lower the valuation.

Accordingly, we can see that SIA's present valuation, on the premise of profit yield, is particularly lower than the five-year normal.

In outline, we can contend that SIA is as of now exchanging at a generally reasonable valuation when contrasted with its five-year history.

All things considered, the low valuation may not be ridiculous, particularly since the organization as of late reported a weaker quarterly execution, which can be found here.

Accordingly, financial specialists are reminded that valuation is by all account not the only criteria to concentrate on. Truth be told, it will be similarly, if not more, vital that financial specialists have a decent handle without bounds prospects of SIA before contributing their capital.

No comments:

Post a Comment